Contracts are undertaken to customer’s requirements, which is generally of constructional. For example, construction of buildings, ships, Bridges, Roads, etc. In all the above cases, contract account is opened. A unique number is allotted to each contract and a separate account is maintained for each individual contract.

Following are the important features of a contract accounting −

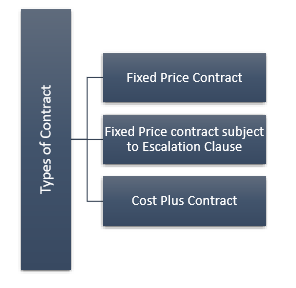

There are three types of contracts, as depicted in the following figure.

Recording of each contract will be done as under −

Cost of “Material” will be debited from the contract account in the following manners −

Contract account will be credited −

Amount will be transferred to Profit & Loss account −

Labor or wages directly charged to concerned contract account and outstanding wages should be debited from the contract account.

In addition to material and labor, all other expenses, which are directly attributable to the specific contract account are called direct expenses and will be debited from the contract account.

Following are the two methods for charging value of Plant & machinery to a contract account −

a) Contract account will be debited with the full value of Plant & Machinery −

Contract A/c Dr (With full value)

To Plant & Machinery A/c (With Full Value)

Contract account will be credited with the depreciated value of Plant & Machinery at the end of the contract −

Plant & Machinery A/c Dr (with Depreciated Value)

b) Contract account will be debited with hourly rate of Depreciation −

This is much better and scientific approach as compared to the first method. On the basis of time, contract will be debited with hourly rate of depreciation.

The expenses, which cannot be directly charged to such contract are known as indirect expenses.

On the basis of some percentage, these expenses may be distributed among several contracts. For example, charges of supervisor, engineer, administrative expenses etc.

When a main or prime contractor assigns some specific work to another contractor as part of the main contract called as sub contract. Sub-contractors are paid by the main contractor. Sub-contractors normally do some specialized work, in which they are specialized. Charges paid to the sub-contractor will be shown in the debit side of the contract account.

Any additional works in addition to the main contract, done by contractor as per the requirement of the Contractee, may be charged to same contract account. However, in case where volume of the extra work is not substantial; so, the amount received in lieu of that extra work should be added to the contract price.

In case where extra work is of substantial amount, a separate contract account should be prepared, as explained above.

During the period of contract, Contractee has to pay sums of amount to contractor especially where a contractor is engaged in a big and long term contract. This amount is paid on the basis of certification of work done by surveyors or architects on behalf of the Contractee, who certified the value of the work done by the contractor.

Usually, some percentage of the certified amounts is paid by Contractee and the balance amount called as “retention money.” The retention amount remains with the Contractee until the work is completed to safeguard and keep in favorable position. Completed work, which is not certified is called “uncertified work.”

Following accounting procedure should be followed after getting certificate −

a) Contractee personal A/c Dr

b) Contractee personal A/c Dr

Retention Money A/c Dr

c) Under this method, any amount received from the Contractee till the completion of contract will be crediting to Contractee’s personal account debiting cash/bank. Amount so received will represent advance received from Contractee and will be shown as (work in progress less advance received) in the Balance sheet.

Actual ascertainment of the cost is possible only after fully completion of the contract. Therefore, it is not possible to know the profit or loss on contract till it is completed.

However, following principles are adopted to estimate profit on uncompleted contracts −

Note − In case of any loss that should be transferred to Profit & Loss account.

Uncompleted contracts at the end of the financial year, which are known as work-inprogress will be accounted as −

Please prepare a Contract Account, Contractee Account and Extract of Balance sheet from the following information as received from M/s “Solid Building Contractor’ for the period 01-04-2013 to 31-03-2014.

| Particulars | Amount |

|---|---|

| Contract Price | 18,000,000 |

| Material Issued to contract | 3,060,000 |

| Wages & Salary | 4,800,000 |

| Plant used for Contract | 900,000 |

| Other Miscellaneous Expenses | 300,000 |

| Cartage paid on Material | 60,000 |

| Loss of Plant at site | 180,000 |

| Plant returned to store on 31-03-2014 | 120,000 |

| Loss of Material at site | 150,000 |

| Material in hand at site on 31-03-2014 | 138,000 |

| Cash received 80% of work certified | 7,680,000 |

| Uncertified work | 60,000 |

| Depreciation on Plant | 15% |

| Profit transferred to Profit & loss account | $\frac>$ |

M/s Solid Building Contractor

Contract Account

(For the period 01-04-2013 to 31-03-2014)